Exchange of information

Convention on Mutual Administrative Assistance in Tax Matters

Last updated: September 2023

The Convention

|

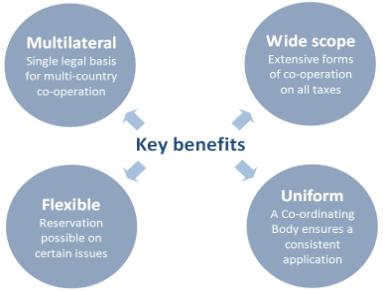

The Convention on Mutual Administrative Assistance in Tax Matters ("the Convention") was developed jointly by the OECD and the Council of Europe in 1988 and amended by Protocol in 2010. The Convention is the most comprehensive multilateral instrument available for all forms of tax co-operation to tackle tax evasion and avoidance. The Convention facilitates international co-operation for a better operation of national tax laws, while respecting the fundamental rights of taxpayers. It provides for all possible forms of administrative co-operation between states in the assessment and collection of taxes. This co-operation ranges from exchange of information, including automatic exchanges, to the recovery of foreign tax claims. Since 2009, the G20 has consistently encouraged countries to sign the Convention including most recently at the G20 summit in Buenos Aires in 2018 where the communique stated "All jurisdictions should sign and ratify the multilateral Convention on Mutual Administrative Assistance in Tax Matters." The text of the amended Convention is available in English, French, German (unofficial translation), Spanish (unofficial translation) and Portuguese (unofficial translation). 147 jurisdictions currently participate in the Convention, including 17 jurisdictions covered by territorial extension. This represents a wide range of countries including all G20 countries, all BRIICS, all OECD countries, major financial centres and an increasing number of developing countries. |

22/03/2023 - Deputy Secretary-General Mr. Yoshiki Takeuchi and Mr. Cao Anh Tuan – Deputy Minister of Finance of Vietnam |

The co-ordinating body

|

In accordance with Article 24(3) and (4) of the Convention, the Co-ordinating Body is responsible for monitoring the implementation and development of the Convention, including:

The Co-ordinating Body is composed of representatives of the competent authorities of the Parties to the Convention and includes the competent authorities of territories to which the Convention applies. The Co-ordinating Body is led by the Chair and three Vice-Chairs. The current officers are:

The Co-ordinating Body is assisted in its tasks by the Secretariat of the OECD. |

|

Process to become a party

- Process to become a Party to the amended Convention

- A Toolkit for Becoming a Party to the Convention on Mutual Administrative Assistance in Tax Matters (OECD, 2020)

MULTILATERAL COMPETENT AUTHORITY AGREEMENTS FOR THE AUTOMATIC EXCHANGE OF INFORMATION

The Convention on Mutual Administrative Assistance in Tax Matters (the "Convention"), by virtue of its Article 6, requires the Competent Authorities of the Parties to the Convention to mutually agree on the scope of the automatic exchange of information and the procedure to be complied with. Against that background, the Multilateral Competent Authority Agreement on the Exchange of CbC Reports (the "CbC MCAA"), for the automatic exchange of Country-by-Country Reports, and the Multilateral Competent Authority Agreement on Automatic Exchange of Financial Account Information (the "CRS MCAA"), for the automatic exchange of financial account information pursuant to the Common Reporting Standard, have been developed.

Compare your country

Discover the international state of play with an interactive map presenting key indicators and outcomes of the OECD work on international tax matters, with over 150 countries and jurisdictions:

LATEST UPDATES

- 13/09/2023 - Viet Nam deposits instrument of ratification for the Multilateral Convention on Mutual Administrative Assistance in Tax Matters

- 07/09/2023 - Papua New Guinea deposits instrument of ratification for the Multilateral Convention on Mutual Administrative Assistance in Tax Matters

- 22/03/2023 - Viet Nam joins Multilateral Convention to tackle tax evasion and avoidance

- 11/07/2022 - Honduras joins multilateral Convention to tackle evasion and avoidance

- 07/07/2022 - Madagascar joins multilateral Convention to tackle tax evasion and avoidance

- 11/08/2021 - Maldives, Papua New Guinea and Rwanda join multilateral Convention to tackle tax evasion and avoidance

- 29/09/2020 - Multilateral Convention to tackle tax evasion and avoidance continues to expand its reach in developing countries, as Botswana, Eswatini, Jordan and Namibia join

- 29/07/2020 - Global Forum Secretariat delivers new toolkit to help countries become Party to the Convention on Mutual Administrative Assistance in Tax Matters

- 22/07/2020 - Kenya deposits instrument of ratification for the multilateral Convention on Mutual Administrative Assistance in Tax Matters

- 03/06/2020 - Thailand joins international efforts against tax evasion and avoidance

- 30/01/2020 - Togo joins international efforts against tax evasion and avoidance

- 27/11/2019 - Benin, Bosnia and Herzegovina, Cabo Verde, Mongolia and Oman join the most powerful multilateral instrument against offshore tax evasion and avoidance

- 03/10/2019 - Montenegro joins international efforts against tax evasion and avoidance

- 02/09/2019 - Ecuador and Serbia deposit instruments of ratification for the multilateral Convention on Mutual Administrative Assistance in Tax Matters

- 13/06/2019 - Serbia joins international efforts against tax evasion and avoidance

- 25/04/2019 - Dominica joins international efforts against tax evasion and avoidance

- 12/02/2019 - Mauritania joins international efforts against tax evasion and avoidance

- 29/11/2018 - Jamaica deposits instrument of ratification for the multilateral Convention on Mutual Administrative Assistance in Tax Matters

- 29/10/2018 - Ecuador signs the multilateral Convention on Mutual Administrative Assistance in Tax Matters

- 27/07/2018 - Antigua and Barbuda becomes the 125th jurisdiction to join the most powerful multilateral instrument against offshore tax evasion and avoidance

- 05/07/2018 - Major enlargement of the global network for the automatic exchange of offshore account information as over 100 jurisdictions get ready for exchanges

- 02/07/2018 - Former Yugoslav Republic of Macedonia signs the multilateral Convention on Mutual Administrative Assistance in Tax Matters

- 22/06/2018 - Vanuatu joins international efforts against tax evasion and avoidance

Related Documents

- Annexes - Convention on Mutual Administrative Assistance in Tax Matters

- Rules of Procedure of the Co-ordinating Body

- Explanatory Report of the Convention on Mutual Administrative Assistance in Tax Matters as amended by the 2010 Protocol

- List of Declarations, Reservations and other Communications

- Original Convention on Mutual Administrative Assistance in Tax Matters: Text and Explanatory Report

- 2010 Protocol Amending the Convention on Mutual Administrative Assistance in Tax Matters